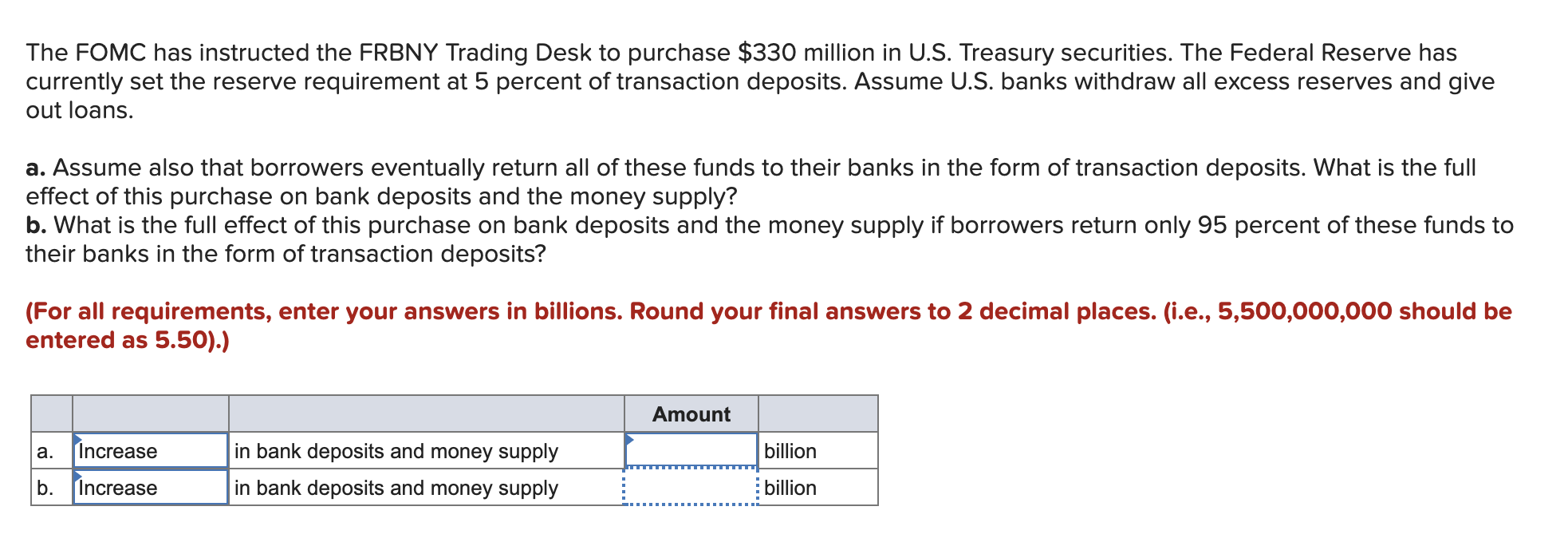

-

HER FINNER DU OSS:

Bondistranda 29E, 1386 ASKER

28 Jan. 2025

An inventory are a monetary signal one loan providers use to put the rate to have Case loans

To have control off a factory-created domestic, it is informed you very first present a sensible thought of how much you can afford to spend to your a house. You ought to jot down obvious and you can particular desires you may have having your residence, and you may considercarefully what is essential and you may what’s optional for you. Thought the real and you may you’ll be able to will set you back of homeownership, also homes lease or pick, financial, insurance policies, taxation and you can repair. Having help from MHIA and you will the constituent participants, you will be able and work out voice decisions in the techniques.

After everything is signed, next actions will be the design of your property and its delivery and installations. Read More

18 Jan. 2025

Repay Our home Mortgage or Put money into Property? –

Whatsoever, it is our biggest loans. It’s a basketball and you can chain, dragging you off because of the legs, shackling that costly repayments for a long time. Thus, it’s a good idea that every some body have to repay it as fast as possible.

Would be to property owners repay the home loan completely in advance of they consider other investment, such as to acquire investment property otherwise committing to offers?

For a few people, this could add up. When you yourself have a very reasonable exposure character, is anticipate your earnings going down afterwards or indeed there are also compelling reason we want to rid yourself from your own home loan financial obligation, this may be is the right way to go.

But when you prevent purchasing since you need certainly to pay back your residence loan basic, you pay a giant prices.

This is just a means of claiming: just how much will it cost you to attend ten or 20 or even thirty years first spending?

Think it over like that: for folks who ordered a house inside Questionnaire 10 years back, and you can waited unless you got it totally paid down offer before you committed to assets, you’d still be waiting to pick a unique funding. In reality, you’ll still be 5 years, 10 years if you don’t next from purchasing it outright.

However, if you would made use of the your guarantee to get an enthusiastic investment property 3 or 4 years ago, you would provides 2 quality possessions property which have both gone through an enormous development spurt.

Their riches was much better with dos functions than it are which have 1, though you take on a great deal more debt.

One loan places Demopolis to most useful finances is the possibility pricing you overlook, for individuals who wait until your home is totally reduced so you can dedicate.

Over the years, I’ve seen a familiar pattern enjoy out in you to definitely beginner some body don’t design their personal debt precisely and you may end up with financing factors that do not suit them otherwise you to definitely restriction their credit potential

Just how do a trader play with their property equity safely, it does not feeling the life and you can makes it possible for get a home (if you don’t make a portfolio from attributes) at the same time? Read More

10 Dec. 2024

I became certainly not willing to stop trying obligation with the profit early on

Thankfully, there were loads of other ways locate right back our very own closeness basic. I happened to be a first-classification nag and you will watched my better half retreating then and further off me personally. Counseling just seemed to ensure it is bad. I then discovered the fresh six Intimacy Experience, hence made my relationship playful and you will intimate once again.

I can not wait for one to have that also. I’ll show you just how in my upcoming webinar: Ways to get Value, Reconnect and you may Step up Your Love Lifetime. You can sign up for 100 % free at

We usually do not be resentful, but I can’t frequently assist me personally

I nag him as the Personally i think including he will become complacent in the which low spending employment and keep maintaining it away from benefits despite having a keen MBA. He states he will look for things ideal hence it simply to loans Elizabeth CO carry inside the a salary however, the guy as well as told you he would be to provide this place half a year as they are purchasing date into him. I didn’t this way believe after all. The organization is employed to help you being good springboard for all those looking going higher. I am worried we are mismatched for the monetary goals and you can desires. I like finer some thing and you will he is shorter repair however, informs me would like to end up being well off someday. The guy originates from a rich family of highest earners and you will upcoming heredity as well however, life style very terrible atm out-of my personal professor income is never ever in which I needed to finish right up. The I could remember is actually divorcing your in spite of the fear and soreness regarding making him. I can not determine if his bundle is too obscure to own their community.

Christina, We listen to how scary it is to think the husband’s top-notch choice. Read More

28 Nov. 2024

Point 206 away from label II of the Operate from Oct fifteen, 1982 (Club

[Source: Section 2[13(g), earlier 13(f)] of one’s Act off September 21, 1950 (Pub. 797; 64 Stat. 889), productive Sep 21, 1950, given that redesignated because of the point 113(m) away from name I of the Operate of October 15, 1982 (Pub. 97–320; 96 Stat. 1474), effective October fifteen, 1982]

09 Oct. 2024

Just what Tax Variations Would you like Out of your Lender?

In most cases, you could potentially deduct new entirety in your home financial notice, although full matter depends on the fresh big date of your home loan, the amount of the mortgage, and exactly how you may be using the continues.

Now inside your life if you possibly could score a taxation deduction on your house guarantee financing, you will be wanting to know though you ought to. Of course, if your house security mortgage useful your home developments qualifies, you will need to assess the complete financial notice whatsoever monthly repayments are manufactured. If your allowable expenses – for instance the next mortgage attention payments – is higher than the product quality deduction to your latest tax year, it could be well worth saying.

That’s worth doing only when your allowable expenditures soon add up to more the level of the product quality deduction to your 2020 taxation seasons:

- $24,800 to have married couples filing together.

- $a dozen,eight hundred getting single filers or married couples submitting separately.

- $18,650 to own direct regarding house.

Before TCJA from 2017, all the domestic security financing was basically income tax-allowable, long lasting. Home guarantee fund are no stretched allowable if for example the financing is actually used private items like holidays, university fees, credit card debt, trucks, attire, an such like.

So you can meet the requirements, you should establish the way you used the money to allege this new HELOC desire income tax deduction. For example getting invoices of all product, labor, and other will cost you obtain to help you upgrade the house or property, company deals, and just about every other documents that displays the latest suggested use of the funds, along with your Closing