-

HER FINNER DU OSS:

Bondistranda 29E, 1386 ASKER

22 Jan. 2025

To your $1,000 Welcome Incentive give, $five-hundred might possibly be reduced personally because of the Education loan Coordinator through Giftly

Bank and you will Added bonus disclosure

This is certainly An advertising. You aren’t Expected to Make Payment Or take One Almost every other Step Responding Compared to that Render.

Earnest: $step one,000 for $100K or higher, $200 having $50K in order to $. Getting Earnest, for folks who refinance $100,000 or more by this web site, $500 of $1,000 dollars bonus is provided privately because of the Education loan Planner. Price diversity a lot more than is sold with recommended 0.25% Vehicle Pay discount. Read More

18 Dec. 2024

For more information regarding the express off credit rating represented by HELOCs, select Bank of Canada

(). payday loans Beaverton AL Economic climate Remark and you can Statistics Canada (). The Day-after-day: Federal balance sheet and you may economic flow account, next one-fourth 2016. [Retrieved on line].

Dey, Shubhasis. (2005). Personal lines of credit and you will consumption smoothing: The possibility ranging from playing cards and you may house equity credit lines. Financial off Canada [Operating Papers 2005-18].

For an even more detail by detail dysfunction of your own new recommendations, pick Company out-of Funds. (2011). Backgrounder: Supporting the long-title stability of Canada’s housing market. [Recovered on the internet].

Individuals can obtain an additional fifteen per cent out-of leverage provided they was amortized within the particular term home loan. Get a hold of Office of one’s Superintendent from Loan providers. (). B-20 Tip: Domestic Mortgage Underwriting Methods and you can Formula. Read More

16 Dec. 2024

Do you have Adequate for Settlement costs?

An example

Client A bring a good cuatro% speed, when you are Customer B enjoys an excellent cuatro.25% speed. Both are to find a beneficial $250,000 domestic. Visitors A pays $179,674 inside the notice when you’re Buyer B will pay $192,746. This will be an improvement of $thirteen,072. Then you definitely need certainly to create that payday loans Peterman it focus with the a lot more notice Client B try purchasing brand new settlement costs regarding loan. Funding new settlement costs can make it more difficult to help you be eligible for that loan in addition to high interest rates can mean a more impressive payment, that could force your financial budget. In the event the borrower official certification happen to be strict then the high desire price was problems.

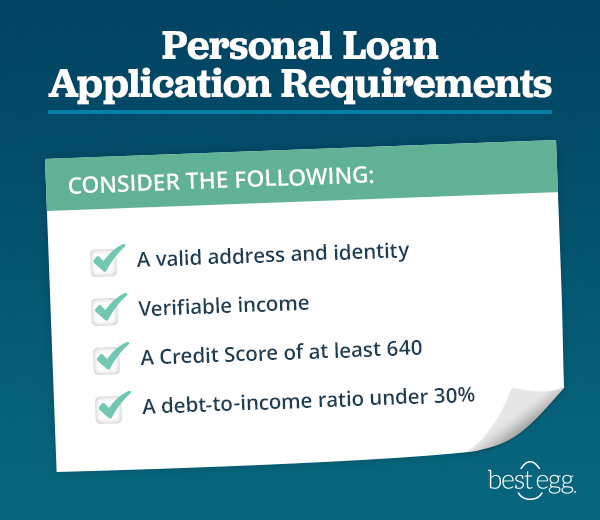

Personal debt so you can Income Proportion

The debt-to-income proportion ‘s the percentage of your earnings that’s going towards spending your debt per month. Of numerous lenders want to see an abundance of 43% otherwise smaller. This shape includes what you are spending on their home loan, and additionally figuratively speaking, credit cards, and any other expenses you’ve got. If you find yourself recognizing a higher rate to fund the fresh settlement costs next this will enhance your payment per month. If you’re boosting your monthly payment, you have got a high loans responsibility.

Even though you is okay to the additional notice and are delivering a no closing rates mortgage, this doesn’t mean you don’t have any currency due within the new dining table. Your own lender could possibly get allows you to provides financing which takes care of customary closing fees, such taxation tape otherwise escrow. Although not, you may still have to pay for one thing generally billed because closing costs, such as individual mortgage insurance policies, transfer charge, otherwise a home taxation. Read More

04 Dec. 2024

Have you been Entitled to a good Loanable Covered Do it yourself Financing?

Shielded Do it yourself Mortgage Explore Times

The secure do-it-yourself loans will be useful in various items. Check out prominent issues where a guaranteed do it yourself financing may be the best solution:

Financial support Highest Renovations: If you are intending a life threatening do-it-yourself project, a secured do-it-yourself mortgage also have the new financial resources you you need. You’re able to fund assembling your project within the an organized and you can manageable way which have one regular installment. For more information, check our home renovation fund.

Enhancing Worth of: Which have renovations, you could potentially probably enhance the value of your residence. A protected do-it-yourself loan has the called for funds to control instance value-adding updates. Read More

15 Nov. 2024

Jumbo mortgage brokers are traditional finance that will be sensed too much become secured by Federal national mortgage association or Freddie Mac computer

Naturally, there is always the danger one things usually do not wade once the structured and you may these types of consumers usually however find themselves in their home whenever highest repayments kick in. Fluctuating mortgage repayments can also be exhausting at best from moments (though some lenders will cap how much cash the payment can be change), and some Arms also have prepayment punishment.

Jumbo Loan

(Mortgage brokers lower than that tolerance have been called conforming money.) This type of constraints can alter depending on your area, and generally are updated periodically; into the 2022, the common cap to own an individual-family home for the majority aspects of the country is actually $647,2 hundred, though into the highest-prices components, one roof you may go up so you can almost $1 million.

Such mortgage brokers can be unlock the possibility of an effective larger or even more magnificent home, property with additional home, otherwise a residence into the a leading-speed city including Nyc. They are also an option to thought for someone attempting to combine several reduced money on one.

That being said, while the jumbo funds are thought high-risk so you can lenders, nevertheless they incorporate alot americash loans Montrose more paperwork, highest borrowing conditions (generally speaking 700 or above), and higher off costs (always 10% or more). Read More